Stablecoins are transforming global payments by offering faster, cheaper, and more accessible solutions with less intermediaries compared to traditional systems like Swift. But setting up a stablecoin payment route involves more than just technical skills. Using stablecoins effectively requires careful planning, financial expertise, and strategic decisions to balance flexibility, compliance, and operational efficiency. First things first, stablecoins come in different types. Some tokens are backed by fiat currencies (either a single currency or a basket), others by cryptocurrencies or commodities, and some are purely algorithmic. Each type requires careful consideration when choosing. Also, not all tokens are issued on the same blockchain, and they may not be available on the blockchains you prefer. This is an important limitation to verify before engaging with them.

In our experience, building a successful stablecoin payment route is a balanced effort: 50% of the process involves technical integrations, while the other 50% focuses on opening accounts and meeting KYC/KYB requirements and regulations with trusted partners in your target jurisdiction. Both are essential to create secure and efficient payment flows. Another important aspect is to start in crypto-friendly regions, where regulations, infrastructure, and market demand support stablecoin adoption. Beginning in the right markets after careful research makes implementation easier and creates a strong foundation for growth.

This guide covers the essentials of creating stablecoin payment routes. We’ll explain the typical payment flow, from stablecoin transfers to settlement in local currencies, and key decisions like choosing between in-house development or outsourcing. You’ll learn how to handle transaction needs, tackle regulatory challenges, and ensure security to create a system that aligns with your business goals. We’ll also cover ways to convert crypto to fiat, including using exchanges, market makers, OTC brokers, banks, stablecoin issuers, PSPs and on/off ramps, explaining the benefits of each option.

Since 2020, DFNS has been helping payment service providers set up stablecoin payment routes by handling the technical integrations. Today, we secure over $1 billion in monthly transactions. PSPs rely on our systems to ensure payment flows are secure, compliant, and automated, allowing businesses to focus on compliance, partnerships, and strategy. Over the years, we’ve gained valuable insights that we want to share to support the growth of the blockchain ecosystem.

By the end of this blog, you’ll have practical tips to refine your roadmap and build a stablecoin solution that is both reliable and well-structured.

Always start with use case in mind

When moving away from traditional payment systems and adopting stablecoins, success depends on understanding your specific needs. Before exploring technical solutions, start by clearly defining your use case. This helps ensure that every decision, from technology to partnerships, supports your business goals. Key factors to consider include:

-

Frequency of transactions: Determine how often you’ll convert between cryptocurrencies and fiat. This affects the automation level and infrastructure you’ll need for on/off-ramps. E.g., daily conversions may require automated systems, while occasional transactions might need simpler ones.

-

Define how often payments are made and whether they are processed individually (gross) or grouped together in batches (netted) as this might have technical implications. E.g., on Ethereum, smart contracts like ERC-4337, also known as “Account Abstraction,” allow batch transactions using bundlers. While this is convenient, it comes with risks you shouldn’t ignore.

-

Simplify the internal user experience by starting with client wallets and progressing to one or more company wallets. Determine whether the company wallets will be omnibus or segregated. Next, map out the flow to the PSP, specifying whether it will come from a single company wallet or multiple segregated wallets.

-

Estimated transaction volumes: Estimate your transaction volumes to determine infrastructure scalability and cost-effectiveness. High volumes might justify custom solutions, while lower volumes could work better with existing platforms. Also, be cautious with tech vendors that charge based on transaction fees or a percentage of volume. These costs can eat into your margins, making it harder to sustain and grow your business.

-

Control and access to funds: Decide how much control over funds you, your partners, clients, or users will have. Options include full custody or shared control arrangements. This decision affects how complex your operations are and how you manage risks. This is also largely a technical discussion that demands a clear understanding and careful analysis of the cryptography and technology being used. It’s important to ensure the tech you choose is audited, tested, compliant, developed by a reputable team, backed by a well-funded or profitable company, and more.

-

Security measures: Define your security needs, especially for high-risk transactions. Advanced technology like MPC wallets, multi-signature wallets or hardware security modules can help mitigate risks. Every crypto PSP should integrate essential tools into their operations, including wallet address whitelisting, transaction policies, 2FA, robust identity and access management, transaction scanning and simulation, etc. While stablecoins can make transactions faster, they also come with new risks that need specific evaluation.

-

Regulatory compliance: Before jumping in, make sure you understand local and international regulations, including KYC, AML requirements, and licensing. While most countries today are relatively open to stablecoins and impose few restrictions, this is expected to change in the coming years. For example, with the MiCA regulation taking effect in Europe in January 2025, Tether has announced it will discontinue support for its euro-pegged stablecoin, EURt.

By addressing these considerations early, you can design a payment flow that is technically reliable and practical for your business. Taking the time to plan now will save effort, time, and costs in the long run.

The basics of a typical payment flow

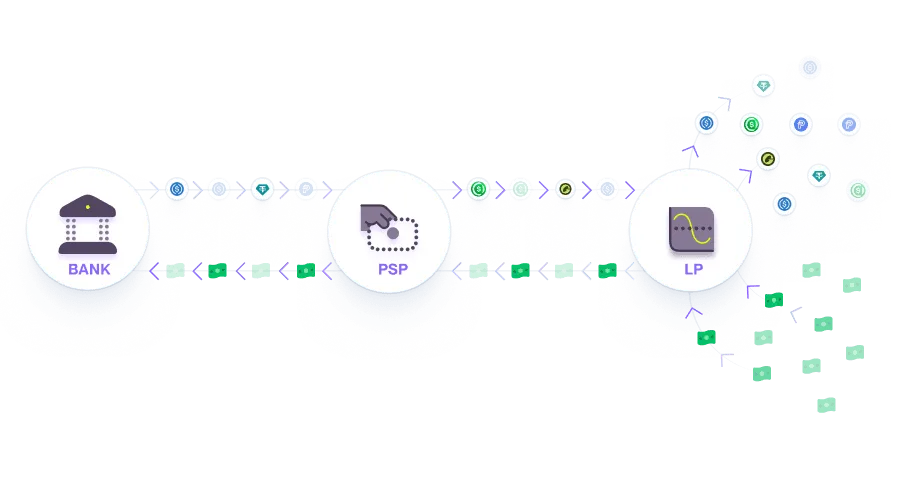

Imagine a bank (X) aiming to improve its payment system by replacing slow and costly SWIFT transfers with faster, more efficient stablecoin payments. Their payment service provider (PSP) facilitates this shift by handling fees and settlement processes with a liquidity provider (LP) for stablecoins.

Here’s how the typical payment flow would work:

- Bank Initiates Transfer: The bank transfers stablecoins (e.g., USDT), received from its clients, to a wallet (e.g., DFNS) managed by the PSP.

- Crypto-to-Fiat Conversion: The PSP works with a liquidity provider (LP) to convert the stablecoins into fiat currency.

- Fiat Settlement: The liquidity provider sends fiat (e.g., USD) to the PSP, which then settles the payment with the bank.

How to approach crypto-to-fiat conversion

Converting stablecoins into fiat isn’t a one-size-fits-all process. The best method depends on your specific needs, like transaction volume, geographic reach, and infrastructure preferences. Thankfully, there are several options to choose from, each with its own benefits and trade-offs. In this guide, we’ll outline the main pathways, using exchanges, OTC brokers, banks, stablecoin issuers, or liquidity aggregators, to help you find the right solution for your business.

Option 1: Exchange Route

- Transfer to Exchanges: Stablecoins are sent from the PSP’s wallet to target exchanges (e.g., Coinbase, Kraken), ideally via native exchange integrations (see here).

- Exchange Offramp: The exchanges allow to sell stablecoins against USD and deposit the USD directly into the Bank’s account.

Option 2: MM/Broker Route

- Stablecoin Conversion via MM/OTC: The PSP converts stablecoins into USD through market makers (MM) or OTC brokers, ideally with a strong footprint in the target geography.

- Direct Offramp to Bank: The PSP sends the converted USD directly to the Bank’s account, bypassing exchanges.

Option 3: Bank Route

- Stablecoin Conversion via Bank: The PSP sends stablecoins to a regulated, crypto-friendly bank which handles the conversion and sends USD back to the PSP.

- Direct Offramp to Bank: The PSP transfers USD directly to the Bank’s account, bypassing exchanges. This can also be done using the PSP’s crypto-friendly bank account.

Option 4: Stablecoin Issuer Route

- Partner with a Stablecoin Issuer: The PSP uses wallets and API integrations to create a KYC-verified account with a stablecoin issuer (e.g. Tether). Stablecoins are deposited into the issuer’s account, and USD is received in return—all through APIs.

- Offramp with the Stablecoin Issuer: USD is sent directly from the PSP’s bank account or the issuer account to the Bank’s account.

Option 5: PSP & On/Off Ramp Route

- Go through PSP or On/Off Ramps: The PSP uses wallets and API integrations to set up a KYC-verified account with a PSP or on/off ramp provider. There are two types of PSP and on/off ramps:

- MM/OTC Aggregation: Consolidates venues from Options 1 and 2.

- Stablecoin Aggregation: Aggregates venues from Option 4.

- Over time, both types of aggregators aim to integrate and unify all options into a single platform for efficiency and scalability.

- Direct Offramp to Bank: The PSP sends USD directly to the Bank’s account.

The distinction between on/off ramps and payment service providers (PSPs) in crypto is important and often misunderstood. On/off ramps, like MoonPay or Transak, help users convert fiat to crypto (on-ramping) or crypto to fiat (off-ramping). These are direct interactions where users complete KYC, use personal accounts, and transfer funds to a merchant’s crypto treasury rather than their own wallet. These transactions function more like funding a treasury or personal exchanges, not traditional payments between unrelated parties. In contrast, PSPs like Bridge, BVNK, and Triple-A handle payments between third parties, similar to traditional payment systems. For example, Bridge enables merchants to receive USD through ACH or FedWire, which can be converted into stablecoins like USDC. The user is unaware of the crypto conversion or Bridge’s role, resembling a payment orchestration model like Stripe.

Which crypto-to-fiat converters to choose

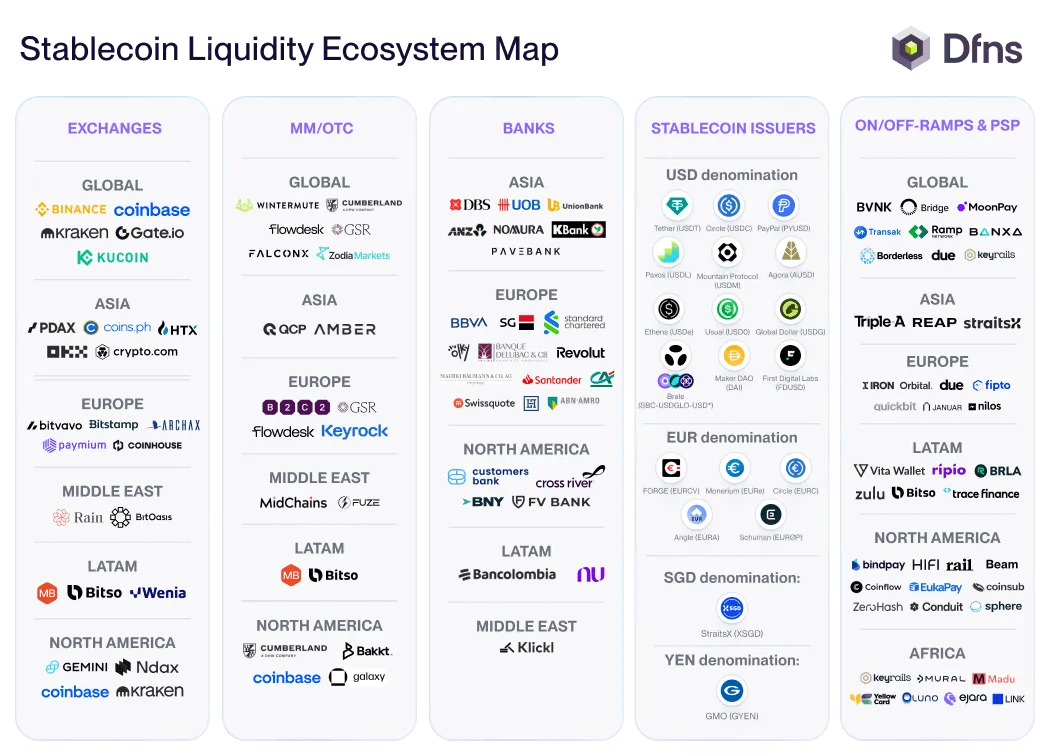

Option 1: Exchanges

In this case, the PSP must create accounts with an exchange and complete the KYC or KYB process. Once that’s done, they’ll receive API keys to connect to their wallet service (e.g., DFNS). With DFNS, you can check the positions and balances of your exchange accounts without leaving the platform. You can also deposit and withdraw directly from those accounts through DFNS.

Exchanges to consider:

- Global: Binance, Coinbase, Kraken, Gate.io, KuCoin

- Asia: PDAX, Coins, Huobi, OKX, Crypto.com

- Europe: Bitvavo, Bitstamp, Paymium, Coinhouse

- Middle East: Rain, BitOasis

- South America: Mercado Bitcoin, Bitso

- North America: Gemini, Kraken, Coinbase, NDAX

Pros:

- Access to a wide range of digital assets and trading pairs.

- Full control over what you sell and at what price while staying within the secure perimeter of your wallet infrastructure for developers, compliance officers, and treasurers.

Cons:

- It’s unlikely you’ll get special rates as an exchange user.

- You’ll need to manage all aspects of order execution and limits yourself.

Option 2: MM/OTC

The PSP needs to open an account with the market maker or OTC broker and complete KYC/KYB verification. Your wallet addresses must be whitelisted by the MM/OTC trading team, which usually takes about an hour. Transfers can be handled manually in direct coordination with the MM/OTC team or automated through the wallet service, like DFNS, with deeper integration. Developing deeper integration typically takes 1-2 weeks, depending on the required features. Most companies opt for manual transfers and settle balances with the MM/OTC desk at the end of each day.

MM/OTC desks to consider:

- Global: Wintermute, GSR, Cumberland/DRW, Flowdesk, FalconX

- Asia: QCPCapital, Amber Group

- Middle East: Midchains

- Europe: B2C2, GSR, Flowdesk, Keyrock

- North America: Cumberland/DRW, Bakkt, Galaxy, Coinbase Prime

Pros:

- Access to better rates by trading in gross.

- Large liquidity pools, ideal for bigger transactions.

- Personalized service with less effort and time on your part.

Cons:

- The process is manual and heavily reliant on the broker, so it’s wise to work with multiple ones.

- Due diligence is crucial to verify the broker’s credibility and regulatory compliance.

Option 3: Banks

The PSP would need to open a bank account and complete the KYB process. Once that’s done, the bank can receive stablecoins from the PSP’s wallets (e.g. DFNS), convert them to USD, and enable the PSP to transfer the funds to the Bank for the final step.

Banks to consider:

- Asia: DBS (Singapore), UOB (Singapore), UnionBank (Philippines), ANZ (Australia), Nomura (Japan), Kasikorn (Thailand), Pave Bank (Georgia)

- Europe: Societe Generale (France), Standard Chartered (UK), Delubac (France), Revolut (UK), Credit Agricole (France), Santander (Spain), BBVA (Spain), HAL Privatbank (Germany), ABN AMRO (Netherlands), Swissquote (Switzerland), Olky (Luxembourg)

- North America: Customers Bank (US), Cross River (US), BNY Mellon (US)

- LATAM: BanColombia (Colombia), NuBank (Brazil)

Pros:

- High compliance and security standards.

- Streamlined process with fewer intermediaries.

- Potentially lower transaction fees due to direct bank involvement.

Cons:

- Can be slow and costly if the bank isn’t directly involved and crypto activities are handled indirectly.

- Banks often rely on OTC brokers (as described in Option 2).

- Many banks are still new to crypto, limiting options in some countries—but this is expected to improve by 2025.

Option 4: Stablecoin Issuers

The PSP creates an account and completes KYC/KYB with the stablecoin issuer. For every stablecoin deposited, you receive one dollar or one euro. The PSP’s wallet provider (e.g. DFNS) can connect smoothly with the issuer’s APIs, enabling automated transaction flows within a secure environment.

Issuers to consider:

- USD denomination: Tether (USDT), Circle (USDC), PayPal (PYUSD), Paxos (USDL), Mountain Protocol (USDM), Agora (AUSD), Ethena (USDe), Usual (USD0), Global Dollar (USDG)

- EUR denomination: FORGE (EURCV), Monerium (EURe), Angle (EURA), Circle (EURC)

- SGD denomination: StraitX (XSGD)

- YEN denomination: GMO Trust (GYEN)

Pros:

- Direct access to liquidity from the source, which may offer better rates.

- Simplified process with fewer intermediaries.

Cons:

- Each issuer provides access to its specific stablecoin only. If you need multiple stablecoins, you’ll need accounts with multiple issuers.

- There is also a risk of loss if the issuer fails, leading to concentration and default issues.

Option 5: On/Off Ramp Providers

The PSP only needs to complete KYB verification with the on/off ramp services. This eliminates the need to open accounts and complete KYB separately with each stablecoin provider. Instead, you gain access to all services through a single API. Some providers, like Bridge or BVNK, specialize in stablecoin liquidity, while others, such as Triple-A, also work directly with merchants and vendors. Wallet services like DFNS can easily integrate with their APIs, enabling stablecoin funds to flow through our platform and convert back into USD.

On/off ramps to consider:

- Global: BVNK, Bridge, Ramp, Moonpay, Transak, Banxa, Borderless

- Asia: Triple-A, Reap, StraitX

- North America: Bindpay, HIFI, Rail, Beam, Coinflow, Eukapay, Coinsub, Zerohash, Sphere

- South America: Ripio, BRLA, Zulu, Vita Wallet, Trace Finance

- Africa: Keyrails, Madu, Yellowcard, Mural, Luno

- Europe: Iron, Orbital, Fipto, Quickbit, Nilos, Due

Pros:

- Simplified process with access to multiple liquidity providers through one API.

- Fewer intermediaries, reducing complexity.

Cons:

- Limited to stablecoins supported by the on/off ramps.

- Possibly higher middleman fees than those charged by on/off ramps.

Some last observations before you go ahead

Building a stablecoin payment route relies on balancing two critical components:

- Technical integrations — Either managed by you or by wallet services like DFNS.

- KYC/KYB accounts — Either set up by you or with your liquidity partners like On/Off Ramps.

The key question is: What should you build, and what should you delegate?

To decide, consider:

- What risks arise if you delegate mission-critical infrastructure?

- How much margin can you absorb while staying competitive with Swift?

- Do you need to acquire or borrow licenses, such as MTLs for US-based transactions?

Your operations are sensitive to change, especially in fast-evolving industries. Locking in a business case or technology upfront is risky because what works today may become obsolete tomorrow. Switching tools frequently is disruptive. Instead, you should choose open, composable infrastructures that can evolve with your needs. Platforms like DFNS wallets-as-a-service (WaaS) provide security, flexibility, and compliance to support blockchain operations, even in a rapidly changing environment.

Key considerations for your decision:

- Regulations: Stay updated on regulatory changes. Financial authorities worldwide (e.g. ESMA, HKMA, CFTC, FSRA, VARA, MAS, etc.) are actively shaping stablecoin policies.

- Liquidity: Ensure your providers have adequate liquidity to support your transaction volumes.

- Integration: Confirm that providers can seamlessly connect with your existing payment systems.

- Fees: Compare transaction fees and costs across providers.

- Security & Compliance: Choose providers with strong security and rigorous KYC/AML standards.

- Risks: Consider concentration, default, and liquidity risks for each provider and the chosen stablecoin issuers.

By carefully weighing these factors, you can build a stablecoin route that supports your business objectives now and in the future.